[00:00:01] Speaker A: Welcome to Crypto Talk Radio, the podcast for everyday investors like you. Visit us on the

[email protected] and now here's your host, Leister.

[00:00:13] Speaker B: Thank you for that, Bailey. And welcome everybody out there in Crypto Talk radio,

[email protected]. hello and welcome, or welcome back. You'll need to forgive me. Allergies are kicking my tail, so I may have an occasional sniffle or occasional cough. I try not to, but it may come out.

Some of it I cannot control.

Allergies are brutal. Because this officially marks the change of weather. It's been this way since I was a kid.

Weather changes. My brother who passed away in 2023, used to say it was a change of weather. Sore throat, that they described it as. What's really happening is that the barometric pressure shift abrupt where I am.

Even in other places where it was more subtle, my body reacts, it reacts very strongly. That's the allergies I refer to. That's sore throat, that's cough, some of which I cannot control.

That's sniffles, that's sinus, that's everything you can think of. It's just a reaction to weather changes and it's powerful. Right now I have an air conditioner or air purifier rather, in this room. And it senses when pollen gets out of control and it tries to do the cleansing, but it runs like continuously. It's bad.

So again, I apologize if it sneaks out. I'll do the best I can to suppress it, but it is difficult.

I got done. I'm just giving personal updates. I got done trying to replace my sump pump.

I have a second one that I was using as a backup because we were getting floods.

And this backup is a beast. He is a beast. So I decided to replace Old Yeller with this guy.

But the piping, something went weird with the piping got seized in there, so I had to kind of jury rig something together MacGyver style. It looks nice, but now I don't have enough water to actually test it. And I don't want to wait until we have a downpour to know it doesn't work because obviously that's kind of bad.

Now I've got a way around it.

It's just not ideal.

I can have. I got one of those roll up folding type of hoses that I can, you know, roll out the window. Cause all the. It's way below ground.

So I do have a plan. It's just, it's not ideal. And I would Love to test the darn thing but I don't want to risk putting a bunch of water in there, having it not work and then have to scramble.

So I'm probably going to wait because I think we're not getting a rain forecast for a week or so. Probably gonna wait till we get a rain forecast close.

Then I'll do the quick test. If it doesn't work then I'll do the roll up as my fallback and just kind of deal with it. Worst case I'll just buy another frickin punk. It's like 200 something dollars and just wire it up that way. And then I want to change the direction of where it sumps out because right now it goes to the front and I don't like that.

We got a couple of bits on crypto, nothing major.

I got a little bit of contradiction I've got to share about some youtubers I was listening to today.

But we'll go through it pretty quick. It's not probably going to be a long episode today.

Coinmarketcap.com we are going to zoom out to the month chart starting with bitcoin, which has a very good upward trend currently hovering around the $81,000 mark. As I record this looking positive and looking like it's got some good momentum. Finally, after a very long time of downward pressure, Ethereum currently hovering just shy of $2,400. As I record this, however, its trend does not appear to be nearly as strong as what bitcoins is doing for one reason or another.

I don't have specific awareness or knowledge about why there's a discrepancy. I simply share that there's a discrepancy between the two and bitcoin seems to be the stronger of them. It's possible it's a fake out. It's possible it's going to go back down. I can tell you it's not attributed to anything about Saylor or Frickin Blackrock. That's not why whatever's happening seems like it's sustained, but time will yet tell. I saw DaVinci Jeremy was talking about, well, if you get into the ETFs, you don't really own the bitcoin. You just get the cash out of it. And he, he hampers on the idea of owning bitcoin and buying bitcoin and getting in, it's going to be a million. You know, he hampers on this and I understand where he's coming from about the idea about not owning it. I don't disagree with what he's saying, but I think he misses certain things. He's talking about the long game, he's talking about the future state. He's talking about a distant, I'll argue future. See, he said himself years ago, I think it was close to 10 years now, ago, he got lucky. He gambled because that's basically what he did. He gambled on it and it happened to win for him. He says he's very wealthy still. I can't say he is or isn't, but let's say he is. He gambled at the right time and he's trying to encourage people to do that again. Well, if we accept that, it probably will be another 10 years before something pans out. The thing I think he's missing is that at the end of the day, you still have to pay bills.

That's going to require cash for the foreseeable future. You're going to need cash to pay those bills. They're not going to take crypto. We can say, oh, this is accepting crypto payments. No, they're not. They're accepting essentially deposits of crypto that then get transformed into fiat and they're paid in fiat. That's what's happening. They're not accepting crypto because if they were, the value of it would be a non issue. And I call that out on DaVinci Germany. It's like if we were really in a world of embracing crypto, the dollar amount equivalency would not matter. It matters because they want the dollar amount equivalency out of it. They want the value out of it. That's not going to change in the short term because everybody's got to get paid. People have bills to pay. The government's not going to do it. Like, until you get to this world, that's not going to happen where everybody doesn't focus on a dollar amount of some kind.

You're not going to really say that crypto is that future.

You're saying, we'll toss some in there now and that's fine. But I don't agree with this idea that you should toss the majority of what you got into it. I don't agree with this idea that there's no value in fiat. I don't agree with some of the concepts he's talking about. I understand why he is, but I don't agree with him.

I think everybody should do what's best for themselves, certainly. But I also, I think people should be smart and understand, including him, bills got to be paid no matter what you can try to borrow against it, sure. But at that point, what are you really doing? You're just shifting in one form of debt to another. At the end of the day, you know, like, I just set up a Amazon card, a store card, with a pretty decent limit, not because I needed it per se, but because if and when there's something I needed to do that exceeds my regular card, okay, I can toss it on there and not worry about it.

I have cash for whatever. But we have limits on cards. I don't want to have to call the bank and say, well, I got to do this transaction. It's over this limit. Have you bumped the limit? It's waste of time. I understand why they do it. I think it's a waste of time. If I do it on that card and the card is in my possession and can't get breached or taken because it's the way it's secured, I think that's a safe way to do that. Could I do the same thing with borrowing its crypto? Certainly. Again, you're just shifting one form of debt to another and it goes back to who has custody of it. If you're borrowing against it, you're not going to have custody of it while you do that. Right. So how's it any different? That's kind of my lens on it.

Again, I don't disagree conceptually with where he's trying to go with it. I just think there's more to it and it's not as simple as he makes it seem from my perspective.

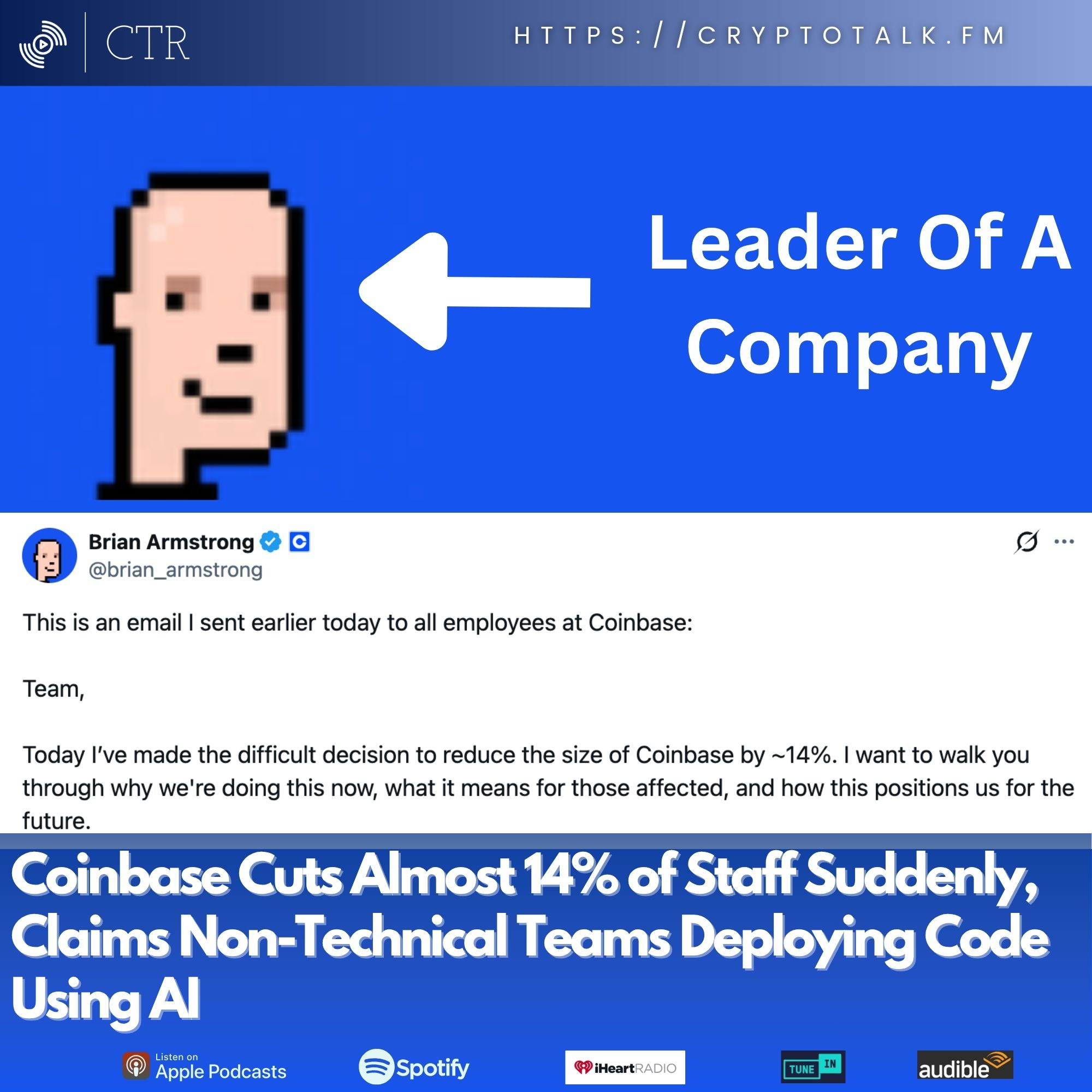

I refer to the next topic person as egghead because of the way he looks. So Coinbase, I don't know if you saw this on the news, but Coinbase did a pretty large layoff. People say it's not large, it's large. Over 14% of staff.

Now, I want to put in some perspective here about the scale of this. Just real quick.

AI was at the dead center of why they said that they were going to do it. Right.

We understood what was going to happen with the AI Rush and all that crap. And this is not the first rodeo for Coinbase. They've done mass layoffs before. And it strikes me that they're a very inefficient, ineffective organization. I was looking up their average salaries.

People were throwing numbers that one of the highest salaries at coinbase was over 600,000 freaking dollars for a non executive.

If you're paying a non executive $600,000, if that's true, you, my friend, don't know how to run a business. Because there's no reason any non executive should be making over 600. I don't care if they're one of your data scientists.

I'm sorry, that is too much frickin money, period, point blank. And I will say that and go to the grave saying it. That means you are not understanding how to pay people. You just are not. Okay, but the average came to something a little bit more reasonable. It's still on the slight high side, but a little bit more reasonable. Somewhere in the neighborhood. $145,000. Okay. For technical people. I can kind of sell it. And they have a history of not cutting the sales and marketing staff, which is who they really need to because those people don't know what the f they're doing. But okay, they're doing a bunch of AI. They were talking about non technical people deploying code to prod. I'm going to warn you to stay away from Coinbase's software dude. Because if they're trusting non technical people to roll AI based software out to prod, you're dealing with buggy shit shows, you're dealing with security issues. I guara damn tee it.

No, you don't do that. You need to have strong technical people, period. And you always will. And people who yolo into it, they're gonna learn a hard lesson. And anybody who supports that, they're gonna learn a hard lesson too.

No, absolutely not.

What you choose to do is what you choose to do. I'm gonna recommend that you don't do that. But what you choose to do is what you choose to do. I decided to run some numbers.

So they're doing a cut and then they're doing some sort of severance package and for the longest tenured employee. So let's say that somebody who was there since the beginning got cut. They got created 2012, okay, so 14 years based on the way their numbers work. The most you could get in a severance, I'm talking straight salary pay is 44 weeks worth of this pay. So there's a little bit for everybody. And I think it was like 12. And then however many years, you get two weeks for every year of service. So it came to, it comes to like max 44 weeks if I go off the average, okay, the average of 145I come to on a weekly basis just shy of $3,400. Just for clean numbers, let's say 3,000 bucks.

Okay, so if it's 3,000 bucks that we can expect clean because it's an average, right? And we multiply that by 44 weeks.

Basically, it comes out to be. If you're that 145, it comes out close to being a year's worth of salary to me.

There's a nice part of getting it all up front, but you're gonna get nailed by the tax man on that money. They're probably gonna hit you about 30% on the tax bracket. Ish.

So you're not gonna walk away with $145,000. It's still a good chunk, but some people who make that much money, they're. They're not living check to check, but they are. They've already kind of invested in stuff where they're not.

Where the money goes quick. It blows quick. You might be asking yourself, well, what about you?

I, you know, I make a pretty decent amount of money, but I have very little expense. The only thing I really have outside of utility bills, basically the mortgage, which I overpay every year or every month rather on purpose to pay it down quick. The mortgage is already close to. Actually it's over a hundred thousand dollars less than what I paid for it. And I just bought the Damn thing in 2024. To put it in perspective, you like $100,000 to the euro.

That's what I'm saying to you, because I understood that interest up front, that's where they nail you. So if you're not overpaying for the first year you own a home, you're doing it wrong. I overpay every single month.

Every single month. It's just that I overpaid more in 2024, and then I tapered off a little bit 2025 and tapered a little bit in 2026, and it'll ramp up again after I get my stuff sorted with the tax deal. So my point is I have enough to overpay every month and still got leftover.

I have utility bills, but I'm offsetting. Most of the biggest is the electric, and I'm offsetting that with all the expenses. I spent about $28,000 on my electrical setup for battery backups and things. I front loaded it. That gives me savings. I have a solar array, so there are days when I have no electric bill because I didn't want to have to deal with a 400, 500, 600amonth bill, especially when it hits summer. I already saw how high it was in the winter.

So my point is, yes, I do, but all I really have is the mortgage.

Every now and then, the utility bill gets to a point it's not that big a deal. And then I have a couple of credit cards, but they're not a lot.

The amount I pay per month is, geez, probably about a fifth maybe of what I make every month. The rest of it goes investing. I'm investing in future, my retirement, the house, the home improvements, etc.

I'm doing things that are designed to get a return because I learned those lessons the last time I bought a house.

Most people that are making in this tier, the six figure tiered above, they don't have the wherewithal to do what I did. Like I have no car payment. You might be surprised. I don't have a car payment. My car is, let's see, 1212 years old, but it only has 66,000 miles.

I bought the damn thing used.

The prior owner didn't take care of it so I had to replace. It's a, it's a plug in electric, plug in hybrid essentially.

So gas. I don't really have a gas charge. I think since I moved here, so we're talking two years now since I moved here. I might have filled the damn thing up full with a 20 bill three times.

I'm not exaggerating. It's a very efficient car and I've done a lot of driving. So I had to drive hours and hours and hours and hours and hours. But it's a very efficient car. I just front loaded it again. I replaced the batteries which the previous owner did not take care of. That was the biggest problem with the car after I took care of that. It drives like a dream. It drives like a brand new freaking car. Despite being 12 years old, I know it's going to last me forever.

That's what I wanted is something where I don't have a. And I had already paid it off. I bought the thing in 2023.

Yeah, 2023. This was after my brother passed because I had bought a different car after my brother. Before my brother passed, I bought a different car. I was going to drive up to see him when I heard he was ill. I couldn't make it because that car had an issue. They couldn't figure out what it was.

So then I bought the car I have now.

After I bought that one, I learned he had passed. That car had registration things and other stuff I had to get sorted out. But once I got all that sorted out, like I said, it's driven like a dream. The ultimate fix that I'm describing happened after I got out here. Once I got here then I found this place online. They were Able to get the battery brand new installed.

I've not had a problem since period.

So I have no car bill, which most people. And I've got a thing I'm going to do on the, on one of the other sister podcasts about how people are just get ripping themselves off on car payments. They're just going up and up and up and up and up. Because in my world, my lens was. I see, okay, you got a car. If you got a car payment, you got to deal with that. You might have college. I actually have student loans. They're going to come due probably next year or whatever. I gotta create a plan, but it's not a lot, but I still have to deal with it.

You might have credit card bills. I actually had three other credit cards.

Four, sorry, four other credit cards. Each one of them were jack offs. So I closed them because I'm like, I can afford you, but I don't need you, but you're not going to do me like that. Screw you, bro. And I kept the, the three I have, which is the Amazon one I just did and then two other ones that are the same bank and they've been fine.

So I don't have a lot of credit card debt.

I have some loans, but they're small and I only did those for home improvement things. And I'm just paying them off over time because I used to work at a credit agency so I understand that the diversity of credit contributes to your score. So the only thing I don't have that I would love to get is a line of credit. And then I got the full suite. I had car loans, they're still on the report. They're going to roll off at some point. Then I'll have to do another car loan at some point. I'm going to have to. Right. I got personal loan, sure. Get a line of credit, sure. Get the credit card, sure. Get the mortgage, sure. I'll consider a home equity line of credit at some point. And then I got the diversity of credit. And then the credit score. My credit score has already been jumping up like crazy. Then goes back to. And the reason I told all that I'm old enough to have gone through cycles of the pain that many of these people that make this kind of money have not hit yet. They haven't learned a lesson yet or they had parents that helped them out. I didn't have parents to help me out. Right. I had to do it myself. I had to hit the grind.

But some of them, they either have, well, somewhat wealthy parents that Gave them a head start. Maybe the parents paid college for them. You know, they had those advantages I lacked. But if they didn't, it just means they've not hit those hard times yet. Since they've not hit them yet, they don't understand what it's like. This amount of money that Coinbase is offering, I guarantee you, for the most of them, it's not going to go that far.

Are they going to have a hard time finding more work? No. If they're good enough to work at Coinbase, I would assume they can probably find more work. But if they're working in the trade that is vulnerable to AI replacement, they might run into the same thing at whatever other company they find.

Meanwhile, I go back to if you're paying people $600,000 a year and you can't seem to avoid laying mass layoffs of people, I think you don't know how to run a fucking business. This does not say that businesses don't lay people off. I'm saying that the frequency, it's like a constant thing with them where they just are constantly cutting people. Tells me they don't know what the fuck they're doing. This guy, he doesn't know what he's doing. Doesn't know how to run a business. Like the guy Ford, same thing. He doesn't know what he's doing either. Where we going? All SUVs, electric.

Butchered the Mustang. Just killed everything that made it stand out. And they're all looking the same. They all look like the Kia is the only thing that stands out. And it's ugly, but at least it stands out. At least they have some sedans, but everybody else is jumping on the bamboo. They all want SUVs. That's not true.

It's just you have certain people and then that allows them to raise the price. And then, of course, goes to the car payment. That's equal to a mortgage, which cuts into stuff like this. It all ties together.

So I don't. I think he just doesn't know what he's doing, is my opinion on it. I don't agree with it. I never have. I've gone through companies, not myself, but I've watched peers at companies get laid off in mass layoffs where they didn't know what they were doing. I actually had a CEO stand up in front of the room and say, we cut too deep, there's not gonna be any more layoffs. And then they did another round of layoffs. And I actually remember people there pissed at the dude cause he's like dude, you straight lied to our faces. You said there wasn't gonna be no more layoffs and they did it again. And then the CFO quit and that's when we knew the writing was on the wall for that company. Something's wrong with this. If you got the CEO actively quitting, you got major problems.

The Clarity act is getting some chatter on social media as well as YouTube. People swearing it's gonna pass, people swearing we're getting close. People swear it's a matter of time and these people flip flop, you know, I said I, I don't see it's getting closer at all. I really don't. It seems like it's got a long way to go because something keeps getting made up. There's something else where they're just making up out of thin air. But now they're talking about something around housing.

Well, I'm not going to go too deep into this one because I want you to go and kind of look into this. I do think it's, it's in your interest to understand exactly what's happening, what's going on. But remember that at first it was about the yields and the stable coins and banks don't want to do that. And then they kind of got a little bit of middle ground. They're still not satisfied but they're kind of, they're, they're, they're trying to get move forward with it.

So then John Kennedy in the house, basically there was, there's some stuff around housing and an act that has nothing to do with it. So what's happening is they're injecting all these other unrelated things as a way to stall progress to make it seem like. Yeah, but this act over here, remember we're supposed to deal with that one. We're not moving forward on that one. If we can't move forward on this one till we move forward on that one. It's all gamesmanship is what's happening. There's other things that are in place.

People concerned about getting, you know, voted out of office and losing their seats because of conservatism or whatever that is.

Concerns about the technology stack and people who write technology and whether they're going to be like arrested if they write certain things. And how can we protect the developers? Can somebody please think of the developers, the whole kyc. How does that going to work? And then you know, how do we deal with anti money laundering if you let this thing go rogue, you know, is it going to increase crime? Like they're, they're Fitting in all of these different things that are not relevant to the passage of this one bill. That's just the way it works. And then remember that the, the House in particular, they, they're on a schedule. So there's times when they're there and times that they're on break and, and so everything is designed to basically slow things down. I honestly believe they're trying to slow things down and they're adding all these barriers and things in front of it designed to slow down the progress because they don't really want it to go forward.

Now the other part of that that you have to think that I think is valid is, remember, if you adopt cryptocurrency in the way that we've butchered it, you are essentially injecting it into the financial market system. So you're saying this is another form of financial transactions.

And by doing that, that means there has to be regulatory oversight stronger than if it's just regular code. Code doesn't have nearly as much oversight.

It has some, but not necessarily as much. And then you talk AI and ethics of AI and it starts to get really problematic when you start combining the world of technology and code with the worlds of finance. And that's also creating barriers that they're trying to overcome where they're not likely to do any of that. Consider that on the, the cryptocurrency pro cryptocurrency side, they still think of it as a form of software, they still think of it as a form of technology.

And at the core it is.

Unfortunately, we butchered it into the financial system. That's its flaw. And they never should have done that. If they hadn't done that and then worked towards this kind of advocacy back then, before it was tied into the public market, this would probably be a non issue because you couldn't make a case about the financial side of things.

However, you wouldn't have a da Vinci journey. You wouldn't have all these wealthy mother fathers who may bank off the early days of bitcoin. It wouldn't exist. Thus, there wouldn't really be a compelling reason for the cryptocurrency side to take off. It only took off because of the financial benefit of it, not because of its technology, the technology underlying. There are certain applications in the mainstream that certainly can support and does support.

I'm saying that those would not have created the same kind of impetus that we saw because of its financial tie in. The, the government knows that. They know that the financial tie in creates an incentive. It also creates temptation which creates criminal elements, which can create risk. And that's what they're trying to oversee. And that's what people are trying to push back on, is they don't want it to be perceived that way. But you have no choice because unfortunately, that's what you've done to the business. And until there's some clarity, no pun intended, you're not going to have any passage of any law that does anything different.

Because unfortunately, there's still a lack of, there's lack of clarity on this deal.

There's also Trump and he's trying to beat the overseas. He's trying to be first and all that. And what does it matter? Because remember, Hong Kong has already been ahead of the game. Dubai has already been ahead of the game. We're already behind it. So it doesn't really matter at this point. Point, I would rather they do it right. And I still say no matter what you're, you need smart regulation, but you're probably not going to get it. You certainly are going to get it. If Donald Trump happens to Donald Trump, you're not going to get it there, guaranteed. You're not the last thing I will cover. And I think it's just a side significance. It's not a major thing. It's just something I wanted to know because you may not have been aware.

Apparently I, I didn't know this, but apparently Grok has its own cryptocurrency wallet. I didn't know this, but this is what I'm told.

The wallet got breached, funds were sent to a bad actor on the base chain.

Apparently I, this is what I'm told. Apparently somebody was able to issue a Morse code command to Grok, which Grok then translated into a transaction that was intended for a different AI bot. And then that bot handled the command to do the sin. So it's like you told this robot to do this command and you built the command in a way that the bot A didn't understand that executing the command was going to be dangerous to it.

And so when it executes the command, it inadvertently includes a command to this other bot that allows it to get breached. It's basically outsmarting what AI is doing. And if you think about what's called the agentic AI concept, the idea that AI is able to respond to commands and do and take action on, on those instructions, etc. I said they're just following your instructions, right? So if you're smart enough with the instructions, this is the kind of thing that happened. Well, think if you were Able to. If you went YOLO into AI, as the kids say, and you had one AI whose job is to oversee a bank vault and another AI whose job is, is to oversee the teller front, which normally is a, should be a strong separation of duty.

And you could pull this kind of thing off there. Somebody could just walk up in there, walk out.

And this just exposes just how stupid it is that they're going YOLO into AI. Now, it wasn't a lot of money, it's a couple hundred thousand dollars. But the point is, this shows the flaws of going all in on AI. AI is not smart enough to contextually understand when to be suspicious. Right. Of stuff. And when you're not smart enough to be suspicious, this thing is going to happen and it's going to happen on a larger scale. And I share it simply so that I can discourage, if I can, people from going YOLO into AI. It's not the right answer. It's never been the right answer. It never will be the right answer.

The better answer is to be smart.

Being smart simply means we should not go YOLO into AI and we should be skeptical of what it does and how it works because it's not mature. The last is because I know there's at least one senator listens to my show CryptoTalk FM. I would really like to see some regulation locking this down. The regulation is very simple. You should never have an AI that can independently execute commands without human intervention. I'm sorry, that, and you should not allow companies to mass lay off people just because of AI. We need to get to a world where we entrust the human element. Back in the industrial age, we need to get back to that because if you don't have strong human oversight into everything that we do, this whole thing is going to crash and burn.

Our society is going to have major problems and you're just going to be looking back, just like with asbestos looking back saying, oh, that was a bad idea back then. Why did we catch it? I'm imploring you guys to really get ahead of this and not allow this to go rogue as what happened in the situation. And be smart and understand that humans are the reason that you can go forward with technology and innovation in a very smart, mature, methodical way. The more you disconnect the humans from this equation, the worse it's going to get because then your humans won't understand how things work. They won't understand why they work. They won't be able to troubleshoot it when they go wrong. And you're going to set yourself up for mass levels of failure, but by all means, feel free to disregard me. I'm just simply trying to warn you before I see that we end up in a horizon zero dawn situation.

Sam.